Many are saying on this blog and elsewhere that the arrangements in the Moyles case were tax evasion, not avoidance. I think what the case actually proves is how meaningless the distinction between those two is, and how nebulous the concept of legal tax abuse has become. As I have already said, an alternative approach to the creation of deliberate tax risk is now needed.

What is do think useful is to share the key paragraph of the decision, which is as follows:

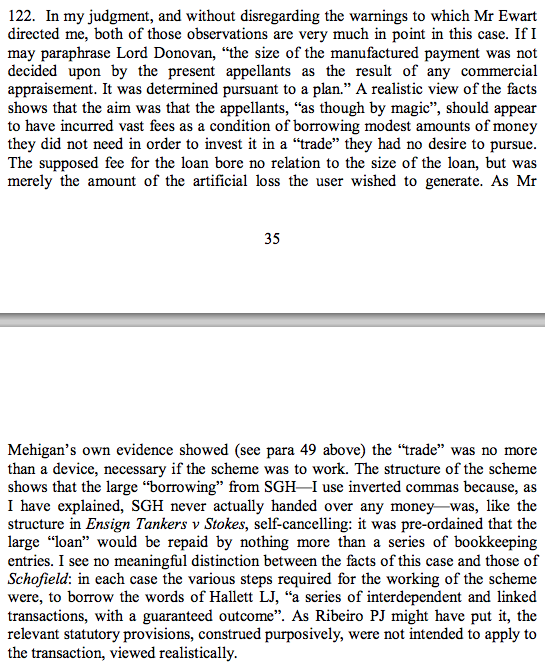

I think when a decision involves the phrase "as though by magic" the Judge is getting as close as he can to saying this scheme has crossed a boundary. That may be one of credibility. It may be something more. He did not say.

What I say is that even if the General Anti-Abuse Rule would have dealt with this case the fact that it has no penalty provisions within it renders it useless to deal with the consequences. I argued for such penalties throughout my involvement with that rule.

I also argued for a broadly based general anti-avoidance principle based on motive and not outcome. This case proves the need for that.

It's time to get real on this issue.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

You can claim all you like, but the fact that this has been addressed under the current rules demonstrates how those current rules are perfectly appropriate and why no random and highly subjective new rule is required….

I will claim all I like

You see, that’s my right

And if people choose to listen that’s their right too

So in other words, this proves nothing.

Yes it does

It proves there is a case to be made for change

And to date there is evidence people are willing to listen

Your disagreement does not prove otherwise

It shouldn’t need a court case to stop a scheme like that. Which shows why the current rules are not appropriate.

Starbucks buys its coffee from a group company in Switzerland, at inflated prices, purely to move profit out of the UK. Which shows why the current rules are not appropriate.

I could go on …

So if you knew of a legal mechanism to lower your tax bill…..you wouldn’t take it?

Similarly, if you were a footballer and your club offered you an increase on your contract, you’d refuse it?

I think you are over complicating what is a very simple matter . A line has been crossed on the basis that Moyes lied on his tax return. He claimed a benefit that he was not entitled to and only qualified because he created fictitious business transactions that never existed. Had he been truthful then the tax benefits would not have been available to him. That is quite simply fraud and all those who participated in this fraudulent scheme should be investigated with a view to prosecution in the criminal courts.

I should also add that we do jot need further legislation as we already have adequate criminal laws to deal with a situation like this .

Can you tell me which?

I am not sure I agree

Presumably the rule under which Moyles is going to be prosecuted…..

But he had taken legal advice he acted legally

At present it is very hard to prove tax crime in that case

I would like to change that but I do not think it simple, unfortunately

“At present it is very hard to prove tax crime in that case.”

So the focus should be on collecting the proper tax without resort to criminal law. It’s much easier and quicker that way.

Whatever happened to Furniss v Dawson?

It’s quicker and easier

But sanction is needed

Furniss v Dawson got a little kicked into touch and the General Anti-Abuse Rule is a poor substitute

In the interests of full disclosure, I disagree with many of Richards’ views on tax policy.

That notwithstanding, as a 19 year old accountant, I spent a day bringing together paperwork to ‘support’ a defence on a Platinum Sponge case. I’ve been a tax advisor for 20 years since, and I can rightly claim that this is the only seven hours I’ve ever spent working on what I have ever since considered to be the wrong side of tax avoidance. It stank, it was shut down, I was happy.

Working Wheels never crossed my desk as a suggestion from a client as an idea to pursue, but many have. In all cases I’ve strongly persuaded them to resist. The one consistent feature is that clients, corporate or personal, have always considered the prospect of success to be many, many times higher than I have. I’ve not yet seen a client pursue a scheme (either against or advice, or without consultation) that worked.

I’m no fan of Chris Moyles either. But the one thing I would suggest to be in point, is that he had no idea what he was entering into. If we’re talking further penalty beyond the denial of scheme operation, and I’ve no complaint that they could be relevant, I’d say that 90% of the time it isn’t the taxpayer in question who should be subject to them.

Richard, let me help you:

The method by which you avoid taxes (National Insurance) through a partnership structure is perfectly legal tax avoidance.

The method by which Moyles tried to manipulate his income to reduce his tax bill was illegal tax evasion.

So the two are very different. (Unless you’re going to accuse yourself of evasion??)

I do not avoid a penny in tax by using a partnership structure

I cannot avoid tax if I do exactly what the law prescribes in the way it intended; it’s a tautological impossibility to do

And let’s be clear, obtuse as it was Moyles took advice that he was avoiding and not evading tax and you know, as I do, that this is why he will not be prosecuted

So you are wrong on both counts

Which is why I usually delete your comments

Quite clearly by using a Partnership structure you pay a lower amount of NIC than if you did not use that structure. Are you denying that?

That’s entirely legitimate tax avoidance, complying exactly with the rules.

It’s somewhat interesting that when other people use the tax rules to legitimately reduce the amount of tax they pay you take a very different view.

Once again, the difference between illegal evasion and legal avoidance…

🙂

No one can avoid tax by making use of a provision specifically provided for in law in the way the law provides for (a critical point)

So I have not, for examples sake, ever said an ISA is tax avoidance. I think it an unnecessary tax relief which is not the same thing.

What you demonstrate is how the tax profession has, I suggest deliberately, debased debate on this issue by debasing the language used

Your arguments are, literally, meaningless as a result

That’s a dangerous thing to argue RM. Google are technically using provisions of tax law (the problem is likely to be implementation with them). Guardian are using provisions in tax law (but you say you don’t like it)

Partners pay less NI than employees.

No it’s not dangerous

The differential is whether the law is being used as intended or not

That’s the key

“No one can avoid tax by making use of a provision specifically provided for in law in the way the law provides for (a critical point) So I have not, for examples sake, ever said an ISA is tax avoidance. I think it an unnecessary tax relief which is not the same thing.”

So taking dividends from a company would also be completely fine even though it avoided NI contributions because, by the same measure, it is a provision specifically provided for in law.

I seem to remember you having a problem with that in the past!…..If partnership escaping NI is fine then so are company dividends!

Taking dividends misrepresents the nature of the income

I have suggested many times how to deal with that

Why does it do so?

If I take say £10K as salary and another £30k as dividends from the profits of my company then why am I misrepresenting the nature of income.

I have a company, I make profits, those profits are distributed as dividends just as the law intends….

You seem to think that the amount of dividends somehow changes the law!….That if I take £50K after a £100k salary then it is within the law but £30k of dividends after £10k of salary and it is not.

Why is taking profits through a partnership instead of a salary OK but not through dividends?

This comment has been posted further to point 5 of the comments policy to which attention is drawn.

Richard Murphy said:

“The differential is whether the law is being used as intended or not”

I’m not sure you are the one best placed to determine what is intended or not. Regardless, if the law is not being used as intended, then the government can change the law.

I have as much right as anyone to suggest change

And none to enforce it

Your problem is?