I've done a lot of work on what accountants call segment reporting over the last few years, largely in connection with the campaign for country by country reporting.

The current IASB approach to segment reporting is found in IFRS 8 which says segments need be reported for the country of incorporation and the rest of the world as a group and on any segmental basis that the key decision makers in the group use, as reflected in internal management reporting.

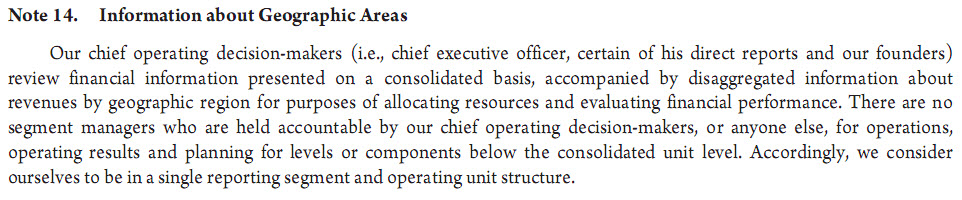

Many in the investment community argued against IFRS 8 because they said it would harm shareholder well-being by reducing the quality of information provided to key managers. In that context note this form the Google accounts for 2007:

Now ask yourself, would you be confident that this board is really in charge of its operations if it does not ask those sort of questions or hold people accountable for these issues or demand information on them? Do you really think they don't do this? Either way governance is compromised.

Do not doubt that IFRS can harm shareholder well being. The case has been proven.

So let's have real segment reporting on real issues, please, and stop this farce.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Richard, whilst I am entirely in agreement with you on the subject of geographical reporting, I do wonder if you are picking on the wrong example with Google. If an entity is mining in Nigeria, clearly there will be local management, employees, contractors and assets IN that country. Google is, afaik, more or less entirely an internet operation based in the United States. It seems perfectly possible that while an internet firm of global reach might want to know how much revenue is being generated from certain geographical territories so they can allocate marketing resources, it doesn’t follow that there is a Vice-President or other manager based in the UK who is responsible therefore – maybe just a centrally sited Marketing Chief.

You can point to the mine in Nigeria – can you point to any asset of Google’s in the UK?

By the way – what a huge coincidence that the ReCaptcha words for this entry are Revenue and Swindle???